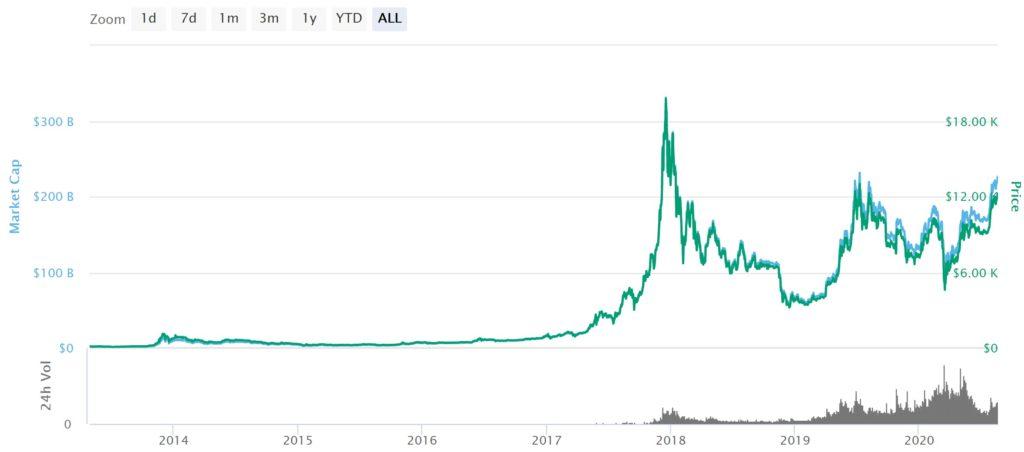

ChatGPT: the pros and cons, and potential relevance to crypto trading

Discover how ChatGPT enhances crypto trading with real-time insights and automation while considering risks like data security and over-reliance on AI.

Gibraltar remains one of the premier jurisdictions for crypto hedge funds

Gibraltar is now the third preferred jurisdiction for crypto hedge funds. Find out why this British Overseas Territory is a top choice for crypto firms!

As compliance costs increase, businesses in Gibraltar face mounting pressure. Explore how stricter AML regulations are reshaping the financial landscape.

Ensure your business is compliant with 6AMLD regulations. TAG Consultancy offers expert AML services, including audits, training, and risk assessments.

Co-founder receives a Non-Executive Director Diploma

TAG Consultancy’s Mark Tewkesbury completes his Non-Executive Director Diploma with outstanding results. His new skills will enhance board performance.

We’ve implemented measures for business continuity during COVID-19. Our team is available remotely via phone, email, and video calls to support clients.